Number of homes currently on the market

Source: National Association of Realtors.

A custom-designed O’Brien Harris kitchen lies at the heart of each residence at One Chicago in Chicago, Illinois.

Jameson Sotheby’s International Realty

Global ripples

Global financial markets are interconnected, so a change in U.S. interest rates affects capital flows in other countries, which in turn can lead to changes in interest rates, says Paulo Fernandes, owner and CEO, Paris Ouest Sotheby’s International Realty in Paris, France.

Europe’s real estate markets have already seen some softening—prices for residential properties declined by 0.3% in the EU in 2023 and 1.1% in the Eurozone, based on data from Eurostat released in April 2024. The largest drop occurred in Germany (7.1%) where economic growth has been slow, while prices rose in Bulgaria (10.1%), Croatia (9.5%), Lithuania (8.3%), Poland (13%), and Portugal (7.78%) due to higher growth.

Any impact felt in France from falling interest rates in the U.S. will be “indirect, complex, and may take some time to materialize,” says Fernandes. “It is difficult to give a precise time frame, as it depends on many factors and how the financial markets and central banks react to the new conditions. The national economy and the state of the political sphere should also be taken into account. These can attenuate or amplify the impact.”

The same applies on the other side of the world. “If interest rates increase, the yen will appreciate, which may impact the number of inbound clients for a bit,” says Mugi Fukushima, director, List Sotheby’s International Realty, Japan. “Overseas clients account for 30% of our clientele, so we’re watching what happens [in the U.S.] quite closely.”

Housing price changes in key European countries (April 2024)

Source: Eurostat

“Some estimates suggest that it takes between one and two years for U.S. monetary policy to have its maximum effect,” says Julian Brown, managing director and founder, New Zealand Sotheby’s International Realty. “However, there is a large degree of uncertainty because the structure of the economy changes over time, and conditions vary.”

Fluctuating exchange rates are important to how attractive the New Zealand property market is. “We have a lot of international interest, especially from the U.S., due to the weaker New Zealand dollar,” says Brown. Buyers who are interested in purchasing homes in New Zealand also have more flexibility when it comes to mortgages, as they can be split into multiple loans at different terms and rates.

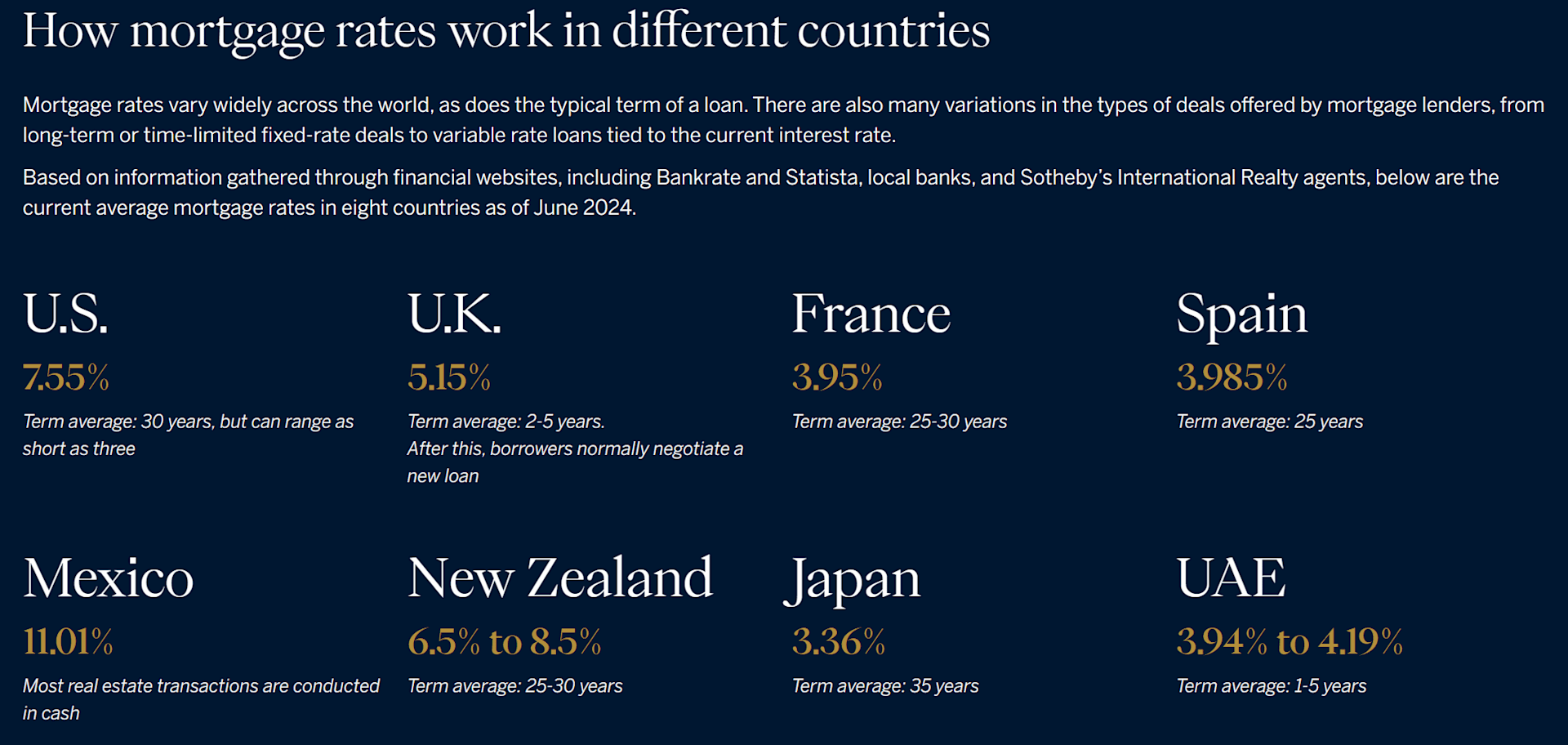

Buyers in the U.S. should also be aware that while 7.55% may be the standard for a 30-year fixed-rate mortgage there now, they vary globally, averaging 3.95% in France for example, or as high as 11.01% in Mexico, where most property deals are primarily done in cash. These rates are influenced by various factors, including the monetary policy of central banks, the local inflation rate, and each country’s economic growth.

“The bottom line is that residential real estate markets in the United Kingdom, Europe, and Asia are influenced by economic growth, while luxury markets are more influenced by local equity markets,” says Chan. “In Asia, Thailand and Malaysia are facing some growth headwinds. After a recession, New Zealand may recover during the second half of the year. South Korea is expected to enjoy stable economic growth. Japan may be slowing down, but is coming back with a booming equity market, which should boost sales of real estate.”

“ THE TIME [TO BUY] IS NOW IF YOU ARE LOOKING AT THE BIG PICTURE IN THE LONG-TERM”

Sam Jenkins, vice president of sales, Jameson Sotheby’s International Realty in Chicago, Illinois